Best 5 AI Gateways for Insurance in 2026: Claims, Underwriting, and Audit Logs

Five AI gateways for P&C, Life, and Health insurance in 2026 scored on NAIC Model Bulletin, NYDFS CL No. 7, EU AI Act Annex III, HIPAA, CO Reg 10-1-1.

Table of Contents

Originally published May 17, 2026.

A regional P&C carrier rolled an AI claims-triage pilot on a Monday and discovered by the end of the week that the gateway it shipped on had been routing the full first-notice-of-loss packet (claimant name, date of birth, Social Security Number, policy number, claim number, body-shop estimate text with Vehicle Identification Number, and a free-text adjuster note) to a consumer OpenAI tier where no Data Processing Addendum was in force, with no claim-file PII redaction layer in front of the model, no audit log of which adjuster prompted what, and no record the carrier could hand the state insurance department when it later asked how the system had declined a coverage extension at 02:00 on a Saturday with no human in the loop. This guide compares the five AI gateways insurance teams should consider in 2026, scored against the NAIC Model Bulletin on the Use of Artificial Intelligence Systems by Insurers (adopted December 4, 2023; adopted in 24 states by May 2026), NYDFS Circular Letter No. 7 (July 11, 2024), the EU AI Act Annex III point 5(c) high-risk insurance use cases (full force August 2, 2026), Colorado Reg 10-1-1 (effective November 14, 2023; quantitative testing in force), the HIPAA Security Rule for health-insurance lines (with the NPRM expected to finalize in 2026), and state-insurance-department record-keeping rules.

TL;DR: The 5 Best Insurance AI Gateways for 2026

Future AGI Agent Command Center is the strongest single pick for an insurance AI gateway in 2026 because it bundles an OpenAI-compatible drop-in, 18+ built-in guardrail scanners covering claim-file PII (SSN, DOB, policy number, claim number, VIN, NPI, MRN), per-virtual-key budgets that map to per-line-of-business spend caps, exact plus semantic caching, OpenTelemetry-native traces that capture underwriter explainability as span attributes, and a self-improving evaluation loop in one Apache 2.0 Go binary you can deploy BYOC inside an insurer’s VPC. Insurance procurement now has to weigh six 2026 events in the same buying cycle: 24 state adoptions of the NAIC Model Bulletin since December 2023, the HIPAA Security Rule NPRM expected to finalize in 2026 (relevant for every health-insurance line), the LiteLLM PyPI supply-chain compromise of March 24, 2026, the announced Palo Alto Networks acquisition of Portkey on April 30, 2026, the EU AI Act Annex III high-risk insurance obligations entering force on August 2, 2026, and the maturation of Colorado Reg 10-1-1 quantitative testing requirements through their first full annual reporting cycle.

- Future AGI Agent Command Center — Best overall. 18+ claim-file PII guardrails (SSN, DOB, policy number, claim number, VIN, NPI, MRN), per-LOB spend caps, OTel-native traces, executable BAA path, BYOC inside an insurer VPC.

- Portkey — Best for insurers that want a managed cost and audit dashboard with per-tenant budget hierarchy. Verify the Palo Alto Networks acquisition timeline before signing multi-year.

- Kong AI Gateway — Best for carriers and brokers already running Kong for policy administration and claims REST APIs that want one control plane across REST plus AI.

- Maxim Bifrost — Best for Go shops where raw throughput on the FNOL real-time fraud-scoring path is the binding constraint and a custom enterprise DPA is acceptable.

- LiteLLM (Enterprise) — Best for Python-first claims-analytics and actuarial teams who want the broadest provider list under a commercial enterprise tier with SOC 2 and SBOM signed releases post-CVE.

The 5 Insurance AI Gateways at a Glance

The pattern is the same across first-notice-of-loss triage, claims adjudication copilots, underwriting decisioning, fraud-special-investigations agents, broker and producer copilots, distribution chatbots, and post-claim subrogation review.

The gateway you pick in 2026 is judged on three controls. Can it redact SSN, DOB, policy number, claim number, VIN, NPI, and MRN before the prompt leaves the insurer’s network hop?

Can it capture model version, prompt template version, output classification, confidence, and the human-in-the-loop disposition as span attributes on every consumer-affecting decision, so the state insurance department’s market-conduct examiner can reconstruct any claim or underwriting decision the Department asks about?

Can it survive a Saturday-night provider 5xx without the claims-time settlement clock ticking past the customer’s expected resolution window?

The seven superlatives read first, then the five-platform shortlist with the one-line reason each made the cut.

| Superlative | Tool |

|---|---|

| Best overall for insurance | Future AGI Agent Command Center: 18+ claim-file PII scanners plus per-LOB spend caps plus OpenTelemetry traces plus self-improving eval loop in one Apache 2.0 Go binary |

| Best open source | Future AGI Agent Command Center: Apache 2.0, single Go binary, BYOC inside an insurer VPC |

| Best for OpenAI-compat drop-in | Future AGI Agent Command Center: base_url swap, no SDK rewrite for the claims-analytics team |

| Best for managed insurance cost dashboard | Portkey: PII anonymization plus four-tier budget hierarchy that maps to lines of business |

| Best when REST and AI share a control plane | Kong AI Gateway: same Kong gateway already in front of the policy administration system handles AI traffic on a separate route family |

| Best for raw throughput on FNOL fraud-scoring | Maxim Bifrost: vendor-published 11 microsecond mean gateway overhead at 5,000 RPS |

| Best for Python-first claims-analytics under a commercial tier | LiteLLM (Enterprise): broadest provider list with a commercial pipeline post-March 2026 CVE |

| # | Platform | Best for | License or pricing model |

|---|---|---|---|

| 1 | Future AGI Agent Command Center | P&C, Life, and Health insurers that want OpenAI compat drop in plus claim-file PII guardrails plus per-LOB budgets in one self-hostable binary; SOC 2 Type II, HIPAA, GDPR, and CCPA all certified, BAA available | Apache 2.0; cloud at gateway.futureagi.com/v1 or self-host or BYOC; AWS Marketplace listing |

| 2 | Portkey | Insurers that want a managed cost and audit dashboard and the most mature semantic cache out of the box | Source available core plus cloud (Palo Alto Networks acquisition announced 2026-04-30, not yet closed) |

| 3 | Kong AI Gateway | Carriers and brokers already running Kong for their REST API plane | Open source plus Kong Enterprise via sales |

| 4 | Maxim Bifrost | Go shops where raw throughput on the FNOL real-time path is the binding constraint | Apache 2.0; Enterprise via sales; custom DPA on advanced compliance tier |

| 5 | LiteLLM (Enterprise) | Python-first claims-analytics teams who want commercial release pipeline assurance after the March 24, 2026 PyPI incident | Apache 2.0 outside the enterprise directory plus a commercial enterprise tier via BerriAI |

Helicone is intentionally not in the ranked list. As of March 3, 2026 it has been acquired by Mintlify; the public posture is maintenance mode while active feature development winds down. Insurance teams already on Helicone should treat it as a planned migration window, not a continued procurement.

How Did We Score These Insurance AI Gateways?

We used the Future AGI Production Gateway Scorecard for Insurance, a seven-dimension rubric.

Insurance adds three pressures most listicles skip: every dimension has to be defensible to a Chief Compliance Officer reading the NAIC Model Bulletin and the relevant state-DOI bulletins, every dimension has to map back to either a Bulletin pillar (governance, risk management, third-party AI systems, testing, transparency), an EU AI Act Annex III article, a Colorado Reg 10-1-1 quantitative testing obligation, or a HIPAA technical safeguard for the health-insurance line of business, and the audit log path has to support per-decision reconstruction for a state market-conduct examination cycle.

| # | Dimension | What we measure |

|---|---|---|

| 1 | Claims-document PII redaction depth (SSN, DOB, policy number, claim number, VIN, NPI, MRN) | Built-in scanner count covering SSN, DOB, policy number, claim number, VIN, NPI, MRN, free-text claimant names; sub-100 ms enforcement; third-party adapter library; whether redaction holds across multi-page claim PDFs the gateway accepts as multipart uploads |

| 2 | Underwriter audit trail with explainability | OpenTelemetry-native traces capturing model version, prompt template version, input feature set, output classification, confidence, human-in-the-loop disposition; adverse-action reason-code path; per-decision reconstruction artifact for state DOI market-conduct examiners |

| 3 | NAIC plus state-DOI compliance coverage | NAIC Model Bulletin (December 4, 2023) governance evidence; NYDFS Circular Letter No. 7 of 2024; Colorado Reg 10-1-1; California Insurance Code 791-ish privacy alignment; Texas Insurance Code Chapter 38; Florida OIR Information Memorandum guidance; whether 24 state adoptions of the NAIC bulletin are reflected in a single audit artifact |

| 4 | HIPAA / HITECH for health-insurance lines | BAA tier eligibility; PHI redaction across the 18 HIPAA identifiers at 45 CFR 164.514(b)(2); six-year audit log retention at 45 CFR 164.316(b)(2); alignment with the HIPAA Security Rule NPRM expected to finalize in 2026 |

| 5 | Deterministic fallback on provider 5xx | Multi-provider failover policy; deterministic fallback path that does not silently degrade output quality; circuit-breaker on consecutive 5xx; ability to route to a self-hosted vLLM or Llama tier without code change; SLO for the FNOL path measured in seconds, not minutes |

| 6 | Per-line-of-business spend caps | Per-key, per-virtual-key, per-model, per-time-window budgets; tag-based routing for Personal Auto vs Homeowners vs Commercial Lines vs Group Health vs Individual Life; cost attribution to a state, an LOB, an agent code, or a claim |

| 7 | Data residency | EU data residency for EU AI Act Annex III workloads; US data residency for NAIC-jurisdiction lines; option to pin a route to a specific provider region; DPA flow-down clarity |

Dimensions 1, 2, and 3 are the three that decide whether the gateway actually keeps an insurer safe in production. The others are confirm-before-signing requirements. The 16-row capability matrix in the next section is the input to this rubric.

We don’t publish a single composite score because the right priority depends on the buyer profile (multi-line carrier versus monoline P&C versus Group Health payer versus broker or MGA versus reinsurer). The decision matrix below the per-tool reviews maps buyer profiles to picks.

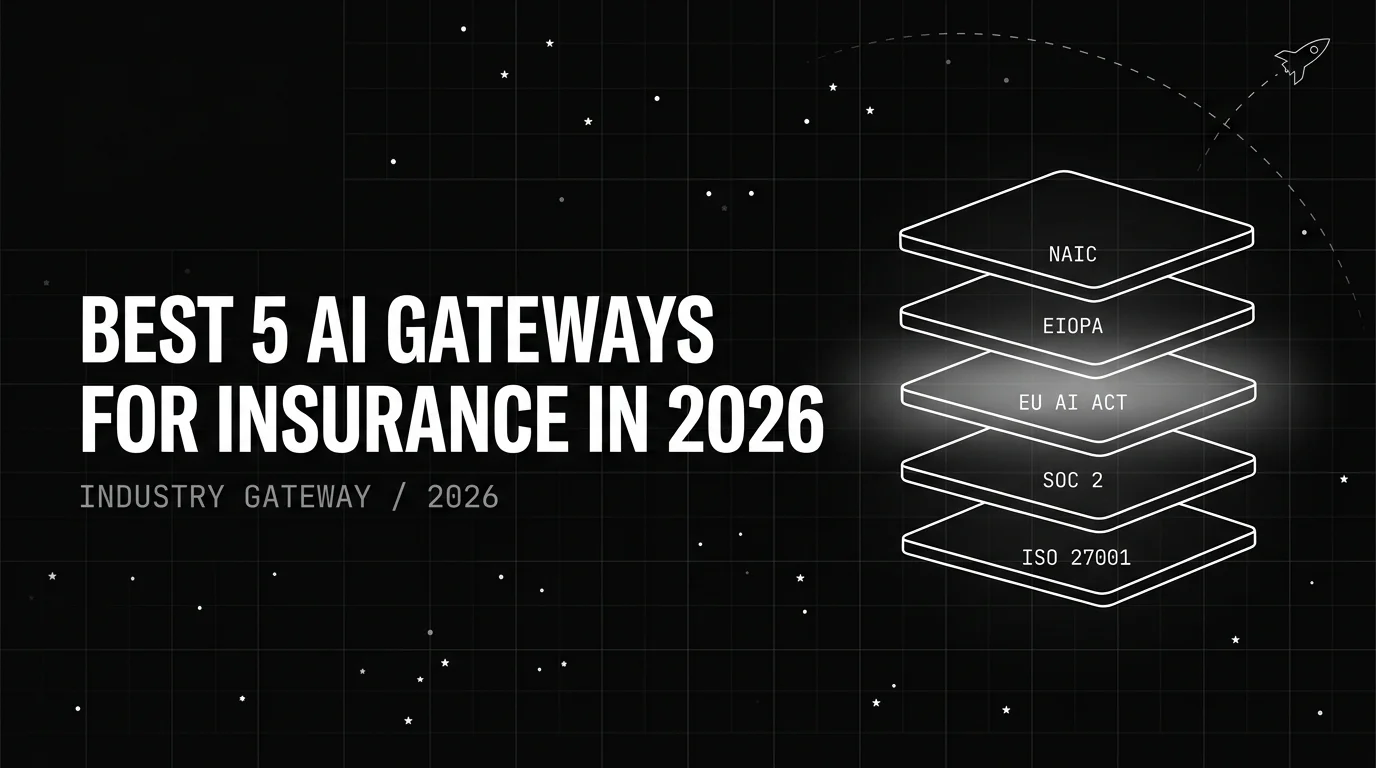

The 2026 Insurance Compliance Stack Actually Demands More Than One Layer

The 2026 insurance AI compliance stack is five layers, and a gateway that handles only one of them isn’t an insurance gateway.

-

NAIC Model Bulletin on the Use of AI Systems by Insurers (December 4, 2023). The Bulletin frames AI governance for every insurer through five pillars: a written AI Systems Program covering governance and risk management; documentation of third-party AI Systems and the due diligence performed on them; ongoing testing and validation; consumer-facing transparency; and senior-management oversight. By May 2026, 24 state insurance departments had adopted the Bulletin verbatim or in close paraphrase, including New York, California, Texas, Florida, Illinois, Pennsylvania, Ohio, and Colorado. The gateway is the practical enforcement point for the third-party AI Systems documentation, the per-decision audit log, and the testing data capture required across the consumer-affecting decision surface (marketing, underwriting, rating, pricing, claim adjudication, fraud detection, post-claim activities).

-

NYDFS Circular Letter No. 7 of 2024 (July 11, 2024). New York’s Circular Letter applies to every authorized insurer in New York and reiterates the obligation under Insurance Law 4224 to avoid unfair discrimination when using External Consumer Data and Information Sources (ECDIS) and AI Systems (AIS) in underwriting and pricing. Insurers must complete a written impact and fairness analysis before deployment, test for disparate impact against protected classes on an ongoing basis, document governance and senior-management oversight, and retain records that allow the Department to reconstruct any consumer-affecting decision. The gateway is the runtime evidence layer for the per-decision reconstruction, with model version, prompt template version, output classification, confidence, and the human-in-the-loop disposition captured as span attributes on every request.

-

EU AI Act Annex III point 5(c) (full force August 2, 2026). Annex III point 5(c) classifies AI systems intended for risk assessment and pricing in relation to natural persons in life and health insurance as high-risk under Article 6. Article 9 risk management, Article 10 data governance, Article 12 automated logging, Article 14 human oversight, and Article 50 transparency enter full force on August 2, 2026. The Commission’s late-2025 Digital Omnibus proposed a Annex III delay to December 2027, but prudent EU insurance buyers continue to treat August 2026 as binding until the delay is enacted. Gateways are the runtime logging surface for Article 12 and the human-oversight checkpoint for Article 14.

-

HIPAA Security Rule plus the NPRM expected to finalize in 2026. Every Group Health and Individual Health insurer is a covered entity under HIPAA. The proposed update to 45 CFR 164.312 removes the addressable-versus-required distinction at 45 CFR 164.306(d) and adds explicit documentation of data flows, vendor relationships, and AI-related risks. Existing BAAs are likely to need amendment when the final rule lands. Gateways with auditable per-request logs and OpenTelemetry-native span attributes are the natural evidence artifact for the data flow inventory the NPRM will require.

-

Colorado Reg 10-1-1 plus the state-DOI testing matrix. Colorado Division of Insurance Regulation 10-1-1 requires life insurers using External Consumer Data and Information Sources, algorithms, and predictive models in underwriting to establish a governance framework, conduct quantitative testing for unfairly discriminatory outcomes against protected classes, document risk-based controls, and produce annual progress reports. The first full annual reporting cycle matured in 2025 and is now a model other state DOIs reference. Texas, California, Florida, Illinois, and Pennsylvania each layer their own record-keeping and market-conduct examination expectations on top, with retention ranging from five years (Florida) to ten years on litigation-touched files (Texas Department of Insurance practice).

A gateway that ships layer 1 and layer 4 but skips 2, 3, and 5 is good for marketing and bad for a state market-conduct examination or an EU AI Act conformity assessment. The five reviews below are scored against all five layers.

What Production Failure Modes the Gateway Is Designed to Prevent

Two failure modes pull insurance AI gateways into procurement scope faster than any feature comparison.

The first is the AI claims chatbot returning PHI or claimant PII to the wrong party. A regional payer ran an internal claims-status chatbot in Q4 2025 that fielded calls from policyholders, providers, and the occasional adverse-claim third party. The chatbot pulled prior claim notes verbatim into its responses for context. When an unauthenticated caller asked about a claim using the claimant’s first name plus the date of service, the chatbot returned the diagnosis code, the procedure code, the billed amount, and the adjuster note. The payer’s notice-of-data-breach analysis took 11 weeks, cost roughly 1.4 million dollars in legal and remediation fees, and surfaced as a state DOI inquiry under the HIPAA Breach Notification Rule. A gateway with claim-file PII redaction at the same network hop and per-role access controls would have blocked the disclosure at the request-response boundary.

The second is autonomous underwriting denying coverage with no explainability. A multi-state P&C carrier ran an AI homeowners-renewal model that produced a non-renew recommendation on roughly 0.4 percent of in-force policies per cycle. Two of those decisions touched a protected class and were challenged. The carrier’s runtime stack captured only the model name and the output label; it couldn’t reconstruct the input feature set, the prompt template version, or the rationale the model used. The state DOI inquiry took 14 months, ended in a consent order, and forced the carrier to manually re-underwrite roughly 28,000 policies at an estimated 47 dollars per file. A gateway with OpenTelemetry-native span attributes and an adverse-action reason-code path would have produced the reconstruction artifact in under five minutes and kept the carrier inside Colorado Reg 10-1-1 and the NYDFS Circular Letter No. 7 record-keeping expectations from the day the pilot left the lab.

The five reviews below are scored on whether the gateway prevents these two failure modes by design, not by integration.

The 16-Dimension Insurance Capability Matrix the SERP Is Missing

Across the five gateways below, Future AGI Agent Command Center leads on combined claim-file PII redaction depth, underwriter audit and explainability surface, NAIC plus state-DOI compliance coverage, and license clarity for insurance. Portkey wins on managed dashboard maturity. Kong AI Gateway wins on REST-plus-AI control-plane unification. Maxim Bifrost wins on raw throughput. LiteLLM Enterprise wins on Python-native provider breadth.

None of the ranked insurance AI gateway posts currently on the SERP ship a 16-column matrix; most stop at four to six columns and skip the NAIC and state-DOI rows entirely.

| Capability | Future AGI ACC | Portkey | Kong AI Gateway | Maxim Bifrost | LiteLLM Enterprise |

|---|---|---|---|---|---|

| Routing strategies (count) | 6 named (15 routing and reliability combined) | 6 plus (4-tier budget hierarchy) | 6 plus (Kong route family) | 6 plus | 6 plus |

| Pricing model | Apache 2.0 plus cloud tiers (Free, Boost 250 USD per month, Scale 750 USD per month, Enterprise via sales); AWS Marketplace | Source available plus cloud; Enterprise via sales | OSS plus Kong Enterprise via sales | Apache 2.0; Enterprise via sales with 14-day free trial | Apache 2.0 OSS plus commercial enterprise tier via BerriAI |

| Language and runtime | Single Go binary | Node plus Python SDKs | OpenResty (Nginx plus Lua) | Single Go binary | Python |

| Supported providers | 100 plus | 250 plus | Major providers via Kong AI plugin family | 1,000 plus models, 10 plus providers | 100 plus |

| Deployment options | Docker, Kubernetes, AWS, GCP, Azure, BYOC, air-gapped, AWS Marketplace | Cloud plus self host plus hybrid plus air gapped | Self-hosted Kong (DB-less or hybrid) plus Konnect | Docker, Helm, in-VPC | pip install; Docker self host |

| Unified API (OpenAI compat) | Yes (base_url swap) | Yes | Yes (/llm/v1/chat route) | Yes | Yes |

| Exact caching | Yes (in memory or Redis) | Yes (Redis) | Yes (AI Semantic Caching plugin) | Yes | Yes (basic) |

| Semantic caching | Yes (in memory, Qdrant, Pinecone) | Yes | Yes (AI Semantic Caching plugin) | Yes | Partial |

| Fallbacks (deterministic) | Yes (multi-provider plus self-host vLLM) | Yes | Yes (Kong upstream balancer) | Yes | Yes |

| Rate limiting | Yes | Yes | Yes (Kong rate-limit plugin family) | Yes | Yes |

| Per-key budgets | Yes (per key, per VK, per model, per window) | Yes (4-tier hierarchy) | Yes (AI rate limiting plugin) | Yes | Yes (basic) |

| Observability | Prometheus /-/metrics plus OTLP traces | Native dashboard plus OTel partial | Prometheus plus Datadog plus OTel plugins | OTel partial | OTel partial |

| Claim-file PII redaction (SSN, DOB, policy number, claim number, VIN, NPI, MRN) | Yes (18+ built-in scanners plus 15 third-party adapters) | Yes (PII anonymization at Enterprise) | Yes (AI Prompt Decorator plus AI Sanitize Data plugin) | Built-in guardrails (specific insurance PII partial) | Via adapters |

| Insurance DPA / BAA coverage on cloud tier | Yes (HIPAA, GDPR, CCPA, and SOC 2 Type II certified; BAA available; AWS Marketplace) | Yes (SOC 2 Type II, ISO 27001; HIPAA BAA at Enterprise) | Yes (Kong Enterprise SOC 2; BAA via Kong Inc.) | Yes (custom DPA on advanced compliance tier) | Yes (LiteLLM Enterprise SOC 2 Type I; Type II in progress) |

| Open source | Yes (Apache 2.0) | Source available | Yes (Apache 2.0 core; Enterprise plugins proprietary) | Yes (Apache 2.0) | Yes (Apache 2.0 outside the enterprise directory) |

| MCP support | Yes (gateway layer plus MCP Security scanner) | Partial | Partial | Yes | Limited |

The shape of the matrix is the shape your buying decision will be: nobody wins every column, and the five columns that matter most for insurance (claim-file PII redaction depth, underwriter audit and explainability, BAA path for health-insurance lines, deterministic fallback for the claims-time path, license and acquisition risk) are where the field separates.

Future AGI Agent Command Center: Best Overall for Insurance AI

Future AGI Agent Command Center tops the 2026 insurance list because it bundles every layer of the insurance compliance stack at the same network hop in one Apache 2.0 Go binary you can deploy BYOC inside the insurer’s VPC.

It loses on out-of-the-box managed dashboard polish to Portkey and on REST-plus-AI control-plane unification to Kong; for buyers whose binding constraint is NAIC-Bulletin-ready routing with 18+ built-in claim-file PII scanners plus per-LOB spend caps plus OpenTelemetry-native underwriter explainability traces in one self-hostable binary, the combined surface still puts it first.

The bundled capabilities are an OpenAI-compatible drop-in, 18+ built-in guardrail scanners (claim-file PII including SSN, DOB, policy number, claim number, VIN, NPI, MRN; PHI for health lines; secret detection; data leakage prevention; hallucination; MCP security), per-virtual-key budgets that map to per-line-of-business spend caps, exact plus semantic caching, OpenTelemetry-native traces, and a self-improving evaluation loop that learns from production failures observed on the insurance workload itself.

Most gateways force a carrier to wire two or three of these together across separate products; Agent Command Center attaches them at the same network hop, with the OSS instrumentation (traceAI, ai-evaluation, agent-opt under Apache 2.0) available for the security team to inspect alongside the hosted Agent Command Center for the operations team. The Protect guardrail layer enforces redaction inside roughly 67 milliseconds end-to-end on the standard policy (arXiv 2510.13351), well inside the claims-time latency budget every adjuster team writes against. The full surface is documented in the Agent Command Center docs and the source ships at the Future AGI GitHub repo.

Best for. Multi-state P&C carriers running claims-triage and renewal-decisioning copilots, Group Health payers running claims adjudication and prior authorization automation, Individual Life writers running underwriting decisioning under Annex III, MGAs running distribution copilots, and reinsurers running submission triage. The OSS plus enterprise dual lets the VP Risk team inspect the instrumentation while the IT Director team operates the hosted plane.

Key strengths.

- OpenAI-compatible drop-in: change

base_urltohttps://gateway.futureagi.com/v1, keep the existing OpenAI SDK code in the claims-analytics service unchanged. - 20+ providers via six native adapters (OpenAI, Anthropic, Gemini, Bedrock, Cohere, Azure) plus OpenAI-compatible presets and self-hosted backends (OpenAI, Anthropic, Google Gemini, AWS Bedrock, Azure OpenAI, Cohere, Groq, Together, Fireworks, Mistral, plus self-hosted via Ollama, vLLM, LM Studio). For insurance, AWS Bedrock under the AWS BAA umbrella, Azure OpenAI under the Microsoft Online Services DPA, and OpenAI Enterprise plus API are the three DPA-eligible upstreams commonly routed for the consumer-affecting decision surface.

- The Future AGI Protect model family for inline guardrails, ~65 ms p50 text and ~107 ms p50 image (arXiv 2510.13351). Protect is FAGI’s own fine-tuned model family built on Google’s Gemma 3n with specialized adapters across four safety dimensions (content moderation, bias detection, security/prompt-injection, data privacy/PII), natively multi-modal across text, image, and audio, a model family, not a plugin chain of third-party detectors. PII coverage spans SSN, DOB, policy number, claim number, VIN, NPI, MRN, free-text claimant names, and the 18 HIPAA identifiers at 45 CFR 164.514(b)(2) for health-insurance lines. A dedicated MCP Security scanner sits alongside and matters after the April 2026 OX Security disclosure of the MCP STDIO RCE class. The same dimensions are reusable as offline eval metrics so the prod policy and the eval rubric stay in sync.

- Per-key, per-virtual-key, per-model, and per-time-window budgets; rate limits; quotas; shadow experiments; tag-based custom properties for per-line-of-business, per-state, per-agent-code, and per-claim enforcement. The natural mapping is one virtual key per LOB (Personal Auto, Homeowners, Commercial Lines, Group Health, Individual Life), with sub-tags for state and producer.

- OpenTelemetry-native traces and Prometheus metrics on

/-/metrics, so the same span attributes feed Grafana, the NAIC Model Bulletin governance evidence collector, the NYDFS Circular Letter No. 7 per-decision reconstruction artifact, and the Future AGI Evaluation pipeline viaspan_idlinking.traceAIinstruments 50+ AI surfaces across Python, TypeScript, Java, and C# (including Spring Boot starter, Spring AI, LangChain4j, Semantic Kernel) OpenInference-natively, and Error Feed. the part of the eval stack, the clustering and what-to-fix layer that feeds the self-improving evaluators, turns those traces into named issues with zero config: auto-clusters related per-LOB failures (50 traces → 1 issue), auto-writes the root cause from the span evidence plus a quick fix plus a long-term recommendation, and tracks trend per issue so claim-triage regressions and underwriter prompt drift get triaged like exceptions. The eval pipeline closes the self-improving loop: production failures feed back into the optimizer, which the gateway re-routes around on the next request class match. - Apache 2.0; single Go binary; Docker, Kubernetes, AWS, GCP, Azure, on-prem, air-gapped or cloud at

gateway.futureagi.com/v1; AWS Marketplace listing for one-click procurement under the insurer’s existing AWS account; HIPAA, SOC 2 Type II, GDPR, and CCPA certified; BAA available for health-insurance lines; RBAC with per-team, per-LOB, and per-region isolation that maps to the NAIC Bulletin governance pillar.

Where it falls short.

- SOC 2 Type II certified (alongside HIPAA, GDPR, and CCPA) rather than published; insurance procurement that requires a finished SOC 2 Type II report on day one should reference the in-progress audit timeline in writing.

- The BAA path is on request rather than included on a published tier; multi-line carriers running Group Health lines should budget legal review time to execute the BAA in parallel with the technical proof of concept.

- Full execution tracing for multi-step autonomous underwriting agents is an in-progress roadmap item in the Future AGI GitHub repo, rolling out alongside the existing gateway-side OpenTelemetry trace export. Carriers running a single-step claims-triage workload land inside the supported surface today; carriers running a multi-step subrogation agent should validate trace fidelity for their workflow.

from openai import OpenAI

client = OpenAI(

api_key="$FAGI_API_KEY",

base_url="https://gateway.futureagi.com/v1",

)

# Existing OpenAI SDK code unchanged from here. The gateway runs

# claim-file PII redaction (SSN, DOB, policy number, claim number,

# VIN, NPI, MRN), per-LOB budget enforcement, and NAIC Model

# Bulletin governance span attributes at the same network hop.

response = client.chat.completions.create(

model="azure-openai/gpt-4o",

messages=[{"role": "user", "content": "Summarise the FNOL packet above."}],

metadata={

"lob": "personal-auto",

"state": "TX",

"claim_number": "**redacted**",

},

)Pricing and deployment. Apache 2.0 single Go binary; cloud-hosted at https://gateway.futureagi.com/v1, BYOC inside the insurer’s VPC, or self-host (Docker, Kubernetes, air-gapped). AWS Marketplace listing for one-click procurement under the insurer’s existing AWS contract. HIPAA BAA available on request for Group Health and Individual Health lines. SOC 2 Type II certified.

Verdict. The strongest single pick if your 2026 insurance infrastructure story is “we want OpenAI compat drop in plus claim-file PII guardrails plus per-LOB spend caps plus OpenTelemetry-native underwriter explainability traces in our existing observability stack, inside our VPC, with a BAA available for the Group Health line and an AWS Marketplace one-click procurement path.”

Insurers that want a managed cost and audit dashboard before writing infrastructure code should evaluate Portkey alongside. Carriers that already run Kong for their policy administration REST APIs should compare against Kong AI Gateway on the control-plane unification axis.

Portkey: Best for Managed Insurance Cost and Audit Dashboard

Portkey is the strongest insurance pick when you want a managed cost and audit dashboard out of the box, the most mature semantic cache in production, and a four-tier budget hierarchy that maps cleanly onto Personal Auto, Homeowners, Commercial Lines, Group Health, Individual Life, and the producer or agent code tag.

It’s what most multi-line carriers reach for when “we need spend control and per-LOB enforcement next week” is the brief, with the caveat that the Palo Alto Networks acquisition announced on April 30, 2026 hasn’t yet closed and is expected to close in Palo Alto’s fiscal Q4 2026 subject to customary closing conditions.

Best for. Multi-line carriers and large MGAs that want fine-grained per-LOB and per-producer budgets, PII anonymization, and a usable cost and audit dashboard without writing a custom exporter, with an acceptable risk appetite for the pending Palo Alto Networks acquisition.

Key strengths.

- Exact plus semantic caching with TTL and similarity-threshold tuning; insurance teams typically see thirty to sixty percent hit rates on internal claims-triage and policyholder-FAQ workloads.

- Per-key, per-virtual-key, per-model, and per-time-window budgets; the most fine-grained native-dashboard hierarchy on the list, mapping cleanly onto multi-LOB tenancy.

- Large adapter library (250+ providers, including private OSS deployments and on-prem Llama variants).

- PII anonymization at the Enterprise tier; HIPAA BAA available at Enterprise for Group Health and Individual Health lines; SOC 2 Type II, ISO 27001, and GDPR audit-log support.

- Usable native dashboard for cost attribution by LOB, state, and feature, which is the lowest-friction NAIC Bulletin testing data artifact.

Where it falls short.

- Acquisition by Palo Alto Networks announced April 30, 2026 and not yet closed; roadmap independence is intact through 2026 but multi-year insurance contracts should reference the integration plan in writing because state-DOI procurement cycles run on three- to five-year windows.

- Observability is dashboard-first; OpenTelemetry export exists but is less first-class than the native dashboard, which makes integration with an existing Splunk or Datadog stack a longer first week.

- Source available core plus closed control plane; air-gapped deployment is available at Enterprise but the control plane setup is heavier than a single Apache 2.0 binary.

- Claim-file PII scanner depth is positioned as PII anonymization rather than a named library covering SSN, DOB, policy number, claim number, VIN, NPI, MRN as discrete scanners; validate identifier coverage against state-DOI examination expectations.

Pricing and deployment. Source available core (self-hosted), commercial cloud control plane, Enterprise via sales; HIPAA BAA included at Enterprise with custom contracts for air-gapped deployment. Verify current pricing on Portkey’s live pricing page before procurement.

Verdict. Most mature managed cost and audit dashboard for insurance AI in 2026, with strong semantic cache and budget hierarchy. Choose with eyes open on the Palo Alto Networks integration; the next 12 months will tell whether the standalone gateway product survives the merger.

Kong AI Gateway: Best When REST and AI Share One Control Plane

Kong AI Gateway is the strongest pick for carriers and brokers that already run Kong in front of their policy administration system, claims management system, broker portal, or any other REST surface and want one control plane covering REST plus AI without standing up a second gateway operations team.

It’s the gateway that wins on API-gateway-grade SLAs because Kong has been the API-gateway parent for the better part of a decade, with a mature plugin ecosystem (AI Proxy, AI Prompt Decorator, AI Sanitize Data, AI Semantic Caching, AI Rate Limiting) that maps AI-specific controls onto the same Kong route family the insurer already operates.

Best for. Multi-state carriers, brokers, and MGAs that already run Kong for the REST plane, want a single team to operate both REST and AI gateways, and prefer plugin-based extensibility over a monolithic AI-specific control plane.

Key strengths.

- One control plane across REST and AI; the policy administration API, claims management API, broker portal API, and AI inference route all run through the same Kong gateway with the same operations runbook, identity federation, and observability pipeline.

- Plugin ecosystem includes AI Proxy (OpenAI-compatible unified API), AI Prompt Decorator (system-prompt enforcement and PII tokenization), AI Sanitize Data (named-entity redaction), AI Semantic Caching, and AI Rate Limiting (per-token budgets).

- Kong Enterprise ships SOC 2, ISO 27001, and audit-log retention paths aligned with the standard state-DOI record-keeping minimum; BAA available via Kong Inc. for the Group Health line.

- Mature deployment story: DB-less, hybrid, and Konnect cloud control plane, with FIPS-eligible builds for carriers operating on FedRAMP-aligned cloud regions.

- Apache 2.0 core; the operations team running Kong open source already knows the runtime, plugin patterns, and route configuration, which lowers time-to-production for a carrier IT team in year one.

Where it falls short.

- The AI-specific scanner library (claim-file PII coverage of SSN, DOB, policy number, claim number, VIN, NPI, MRN as discrete named scanners) is positioned more as a plugin configuration exercise than a built-in scanner library on the scale of Future AGI’s 18+; insurers should write the redaction policy explicitly in plugin config and treat it as code under change control.

- Underwriter audit and explainability surface is built on Kong’s standard logging plus the AI plugin family; per-request span attributes are available but require deliberate OpenTelemetry pipeline setup rather than shipping as the default surface.

- The self-improving optimizer pattern isn’t native to Kong; carriers that want the closed loop should treat Kong as the runtime layer and source the optimizer separately.

- Kong Enterprise pricing rises quickly past the small-broker tier; price the AI plugin family against standalone alternatives at production volume before committing.

Pricing and deployment. Open source Kong gateway plus AI plugin family; Kong Enterprise via sales with SOC 2, audit-log retention, and BAA paths; Konnect cloud control plane available. AWS, Azure, and GCP marketplace listings.

Verdict. The right pick when the procurement constraint is “we already run Kong; we aren’t standing up a second gateway operations team for AI.” Choose Future AGI Agent Command Center when a built-in 18+ insurance-specific scanner library and an Apache 2.0 single Go binary with native OpenTelemetry traces matter more than control-plane unification with the existing REST plane.

Maxim Bifrost: Best for Throughput on the FNOL Fraud-Scoring Path

Maxim Bifrost is the Go-native gateway from Maxim, Apache 2.0, with vendor-published gateway overhead around 11 microseconds at 5,000 RPS, a custom DPA on the advanced compliance tier, and a strong story for the real-time fraud-scoring path that runs alongside first-notice-of-loss on a multi-line property book.

It’s the gateway most often cited when the binding constraint is raw throughput at high concurrency under a custom DPA, especially for carriers running real-time fraud-scoring on physical-damage claims where the decision has to land in seconds, not minutes.

Best for. Go shops, fraud-scoring teams running real-time decisioning on FNOL packets, claims-payment routing engines, and engineering teams whose binding constraint is raw throughput under a custom DPA.

Key strengths.

- Vendor-published benchmark showing roughly 11 microsecond mean gateway overhead at 5,000 RPS on

t3.xlarge, inside the FNOL real-time fraud-scoring budget for most personal-auto carriers (sub-second total decision budget once model inference and network round-trip are included). - Apache 2.0, single Go binary; Docker plus Helm plus in-VPC deployment.

- Custom DPA available on the advanced compliance tier; SOC 2 Type II, ISO 27001, HIPAA, and GDPR audit-log support listed on the public compliance page.

- 1,000+ models from 10+ providers via a unified API surface, useful for carriers routing across a primary commercial model and a self-hosted Llama tier for the high-volume claims-summary path.

Where it falls short.

- Maxim self-ranks Bifrost number one across its own gateway listicles with no published limitations; a trust signal worth weighing when the same vendor’s claims appear in a state-DOI examination risk register.

- Insurance-specific PII redaction is positioned via adapters rather than a built-in named scanner library covering SSN, DOB, policy number, claim number, VIN, NPI, MRN; carriers should validate identifier coverage before relying on the gateway as the redaction enforcement layer.

- The BAA is custom on the advanced compliance tier rather than included on a published tier; Group Health and Individual Health teams should budget more legal review time than for a published-tier BAA vendor.

- Underwriter explainability is available through standard span attributes but not packaged as an insurance-specific audit artifact on day one; engineering teams should plan to build the reason-code path into their own pipeline.

Pricing and deployment. Apache 2.0; Docker, Helm, in-VPC; Enterprise via sales with 14-day free trial; custom DPA on advanced compliance tier.

Verdict. Strong throughput numbers and active engineering velocity, but go-faster isn’t the same as keeping claim-file PII off the wire. Choose Bifrost when throughput is the primary axis and a custom DPA review is acceptable; choose Future AGI Agent Command Center when an executable BAA path, a built-in 18+ scanner library, and a packaged underwriter explainability artifact matter more.

LiteLLM (Enterprise): Best for Python-First Claims-Analytics Teams Post-CVE

LiteLLM is the Python-first proxy that broke open the multi-provider unified API category. It’s Apache 2.0 outside the enterprise directory, ships with 20+ providers via six native adapters (OpenAI, Anthropic, Gemini, Bedrock, Cohere, Azure) plus OpenAI-compatible presets and self-hosted backends, and powers a long tail of internal carrier gateways stood up by actuarial and claims-analytics teams in 2024 and 2025.

After the March 24, 2026 supply-chain incident, the insurance answer is “use the LiteLLM Enterprise commercial tier via BerriAI for a hardened release pipeline with SBOMs and signed releases, or pin to 1.82.6 or earlier on the OSS path and have the carrier hold its own DPA direct to the upstream model provider.”

Best for. Python-first claims-analytics and actuarial teams that already operate a FastAPI or uvicorn surface, want broad provider coverage, prefer a commercial release pipeline post-CVE, and have their own DPA path direct to the upstream model provider rather than relying on a LiteLLM DPA.

Key strengths.

- Broadest provider coverage of any single project on this list (20+ providers via six native adapters (OpenAI, Anthropic, Gemini, Bedrock, Cohere, Azure) plus OpenAI-compatible presets and self-hosted backends), which matters for carriers routing across OpenAI, Anthropic, Azure OpenAI, AWS Bedrock, and a self-hosted Llama tier on the same internal gateway.

- Apache 2.0 outside the enterprise directory; trivial to fork or audit for the carrier security team.

- Virtual keys with per-key budgets; budget alerts; native fit with Python observability stacks already running in the actuarial team.

- Active maintainer community; easy to extend with custom adapters for insurance-specific scanners and an adverse-action reason-code capture middleware.

- LiteLLM Enterprise tier (via BerriAI) ships SOC 2 Type I (Type II in progress), ISO 27001, and a release pipeline with SBOMs and Sigstore-signed artifacts that addresses the supply-chain incident posture.

Where it falls short.

- March 24, 2026 PyPI supply-chain compromise. Versions

1.82.7and1.82.8were published by the TeamPCP threat actor after PyPI publishing tokens were exfiltrated via a compromised Trivy GitHub Action in LiteLLM’s CI/CD pipeline. The malicious packages shipped a credential harvester, a Kubernetes lateral-movement toolkit, and a persistent systemd backdoor; over 40,000 downloads occurred before PyPI quarantined within roughly forty minutes (Datadog Security Labs writeup of the LiteLLM PyPI compromise). Pin to 1.82.6 or earlier on the OSS path; the Enterprise tier shipped under its own commercial release pipeline. - Python runtime; materially slower throughput than Go-binary alternatives at high concurrency, which matters on the FNOL fraud-scoring real-time path where Maxim Bifrost wins on raw throughput.

- The insurance-specific scanner surface is built through adapters rather than a built-in scanner library covering SSN, DOB, policy number, claim number, VIN, NPI, MRN out of the box; carriers should treat the scanner stack as code under change control.

- The OSS distribution doesn’t ship a vendor BAA or vendor DPA; carriers should hold the DPA directly with the upstream model provider on the OSS path.

Pricing and deployment. Apache 2.0 outside the enterprise directory; pip install or Docker self-host on the OSS path. LiteLLM Enterprise via BerriAI for SOC 2, ISO 27001, signed releases, and a commercial support contract.

Verdict. Still the broadest provider coverage on the list, but the March 2026 supply-chain incident shifts the OSS path from “default pick” to “pin commits and audit,” with LiteLLM Enterprise as the recommended commercial path for an insurance team that wants release-pipeline posture aligned with state-DOI examination expectations.

AWS Bedrock and Azure OpenAI as Insurance DPA Fast Paths

The straight cloud route to an insurance-suitable DPA in 2026 is AWS Bedrock under the AWS BAA umbrella (for Group Health and Individual Health lines) or Azure OpenAI under the Microsoft Online Services DPA. Both ship a fast DPA, both are widely accepted by state insurance departments as well-managed third-party arrangements, and both leave the carrier to bolt claim-file PII redaction, per-LOB spend caps, underwriter explainability capture, and the per-decision reconstruction artifact on top.

Most production insurance AI stacks today run an AI gateway in front of Bedrock or Azure OpenAI rather than instead of them. The framing question is whether the gateway adds enough at the same network hop to justify the operational footprint.

AWS Bedrock under the AWS BAA umbrella. Amazon Bedrock and Bedrock AgentCore were added to the AWS HIPAA Eligible Services list effective February 10, 2026; the carrier executes the AWS BAA umbrella once at the account level, and processing of electronic protected health information must use HIPAA-eligible services only (AWS Bedrock security and compliance overview). Bedrock is in scope for ISO, SOC, and CSA STAR Level 2. The gap a gateway closes: Bedrock doesn’t ship a built-in claim-file PII redaction layer, doesn’t ship per-virtual-key budgets across providers (Bedrock budgets are per service), and the OpenAI compat surface in front of Bedrock is on the customer.

Azure OpenAI under the Microsoft Online Services DPA. Azure OpenAI is covered under the Microsoft Online Services Data Protection Addendum for text-based services on Enterprise Agreement, MCA, and CSP procurement paths (Microsoft Learn answer on Azure OpenAI HIPAA eligibility). Azure OpenAI doesn’t retain prompt and completion content for training by default. Two coverage gaps insurance teams hit in practice: image inputs aren’t covered by default (matters for damage-photo workflows on P&C lines), and the Realtime Audio API in preview isn’t yet inside the DPA scope (matters for voice-channel claims intake on personal lines). A gateway in front of Azure OpenAI enforces text-only routing where the DPA doesn’t extend, blocks unauthorized image and realtime calls, and standardizes the audit log across Azure OpenAI plus a non-Azure fallback provider.

The honest take. If your carrier stack is one provider, one region, one product, one LOB, AWS Bedrock or Azure OpenAI behind your application can be enough. The moment you add a second provider (for fallback when the primary returns 5xx at 02:00 on a Saturday and claims-time is money), a second product (claims-triage plus underwriting plus distribution copilot), a second LOB, or a second tenancy (a multi-state book or an MGA program model), the gateway pays for itself in DPA simplicity, claim-file PII redaction consistency, and audit log uniformity.

The DPA Matrix Per Upstream Model Provider

Insurance procurement that picks a gateway also has to pick its upstream model provider, and the DPA clauses (training-on-data, retention default, sub-processor flow-down, image and realtime coverage, BAA path for the Group Health line) differ enough that they belong in the same buying table. Verify each row against the live vendor page before signing.

| Provider | Insurance DPA available | BAA path for Group Health | Procurement path | Training on customer data | Default retention | Image input under DPA | Realtime audio under DPA |

|---|---|---|---|---|---|---|---|

| OpenAI (ChatGPT Enterprise + Edu + API) | Yes (API DPA) | Yes (email baa@openai.com on the API tier) | Standard DPA on API; ChatGPT Enterprise via sales | No (opt-out default on covered tiers) | Configurable; Zero Data Retention available on API | API: yes for text; verify image coverage in BAA addendum | Realtime API not yet inside default BAA scope; verify in writing |

| OpenAI (ChatGPT Free, Plus, Business) | No | No | n/a (consumer surface; not for claim-file data) | n/a | n/a | n/a | n/a |

| Anthropic (Claude API) | Yes, per use case | Yes, per use case | Submit use case and downstream data flow; legal review | No (no training on customer data by default) | API standard retention with delete on request | Yes for text; image inputs covered per use case review | n/a (no native realtime API) |

| Azure OpenAI Service | Yes (Microsoft Online Services DPA on EA, MCA, CSP) | Yes (under the Microsoft Online Services BAA) | Automatic on covered enterprise procurement | No (no training on customer data) | No prompt and completion retention for training by default; abuse-monitoring opt-out path available | Image inputs not covered by default; verify addendum | Realtime Audio API in preview is not yet inside default coverage |

| AWS Bedrock and Bedrock AgentCore | Yes (AWS DPA umbrella plus Financial Services architecture patterns) | Yes (HIPAA Eligible Services list updated 2026-02-10) | AWS BAA umbrella signed at the AWS account level | No (Bedrock does not use customer data to train base models) | No log retention by default; CloudWatch and S3 logging is customer-configured | Multi-modal provider-dependent; confirm at the upstream model | n/a (Bedrock voice agents are a separate service path) |

| Google Cloud Vertex AI (Gemini) | Yes (Google Cloud DPA covers Vertex AI for insurance-eligible services) | Yes (Google Cloud BAA at the organization level) | Google Cloud DPA signed at the organization level | No (no training on customer prompts) | Configurable; default minimal | Image and multi-modal covered per Vertex AI service docs; verify per model | Live API and audio surfaces vary by model; verify each model |

| IBM watsonx.ai (Enterprise plans) | Yes (Business Associate Addendum analogue) | Yes (through IBM Cloud HIPAA-aligned hosting) | Through IBM Cloud insurance-aligned hosting | No on Granite; varies on third-party models exposed through watsonx | Zero Retention Mode available | Model dependent | Model dependent |

The DPA matrix is the per-provider half of the insurance gateway buying decision. The gateway in front of the provider is what enforces the carrier’s own NAIC Model Bulletin and state-DOI technical controls on top: claim-file PII redaction, audit log retention to the state-DOI record-keeping minimum, per-role access, per-virtual-key budget enforcement, and the per-decision reconstruction artifact a market-conduct examiner will eventually ask for.

The 2026 Insurance Gateway Migration and Trust Cohort

Every insurance AI gateway post currently on the SERP is treating these as if they didn’t happen. They did, and they reshape the procurement question for 2026 inside a state-DOI-supervised carrier or a HIPAA-covered Group Health payer.

- Helicone joining Mintlify (March 3, 2026). Helicone acquired by Mintlify; product is in maintenance mode with no active feature development. Insurance teams already on Helicone should plan a migration window, not a continued procurement.

- LiteLLM PyPI supply-chain compromise (March 24, 2026). TeamPCP-attributed compromise of versions

1.82.7and1.82.8via a stolen PyPI publishing token (exfiltrated through a compromised Trivy GitHub Action in LiteLLM’s CI/CD). The malicious package shipped a credential harvester, a Kubernetes lateral-movement toolkit, and a persistent systemd backdoor; PyPI quarantined the packages the same day, with 40,000+ downloads recorded. Pin to 1.82.6 or earlier on the OSS path; rotate credentials accessible to any affected install; the LiteLLM Enterprise tier ships under its own commercial release pipeline. Primary source: the Datadog Security Labs writeup. - Anthropic MCP STDIO RCE class (April 2026). OX Security disclosed an STDIO transport class flaw affecting roughly 7,000 MCP servers and 150 million plus downstream downloads. Insurance gateways routing MCP traffic for agentic claims-triage or distribution copilots are now expected to enforce least-privilege tool access, OAuth 2.1 transport, and Streamable HTTP rather than raw STDIO. Primary coverage: the Hacker News report on the Anthropic MCP design vulnerability.

- Portkey acquired by Palo Alto Networks (April 30, 2026, not yet closed). Acquisition announced; the deal is expected to close in Palo Alto’s fiscal Q4 2026 subject to customary closing conditions. Roadmap independence is intact through 2026; multi-year insurance contracts should reference the integration plan in writing because state-DOI procurement cycles run on three- to five-year windows. Primary source: the Palo Alto Networks press release.

The practical takeaway: for the next 12 months, license clarity, DPA tier definitiveness, BAA path simplicity for the Group Health line, and acquisition independence are part of the insurance AI gateway buying decision. A cheap gateway you migrate off in six months, or one whose DPA pathway is in legal redrafting, isn’t cheap inside a state-DOI market-conduct examination cycle.

Insurance AI Gateway Picks by Buyer Profile in 2026

The buyer profile drives the pick more than the feature matrix does. Multi-line carriers running claims-triage and underwriting decisioning pick Future AGI Agent Command Center for the Apache 2.0 plus built-in 18+ claim-file PII scanner library plus self-improving optimizer combination.

Multi-state carriers running multi-LOB dashboards pick Portkey. Carriers and brokers already on Kong for the REST plane pick Kong AI Gateway. Go shops running FNOL real-time fraud-scoring pick Maxim Bifrost. Python-first claims-analytics teams pick LiteLLM Enterprise.

| If you are a… | Pick | Why |

|---|---|---|

| Multi-state P&C carrier running claims-triage and renewal-decisioning copilots, OpenAI SDK heavy | Future AGI Agent Command Center | OpenAI compat drop in plus 18+ claim-file PII scanners (SSN, DOB, policy number, claim number, VIN, NPI, MRN) plus per-LOB budgets in one Apache 2.0 Go binary, BAA available, AWS Marketplace |

| Group Health payer running claims adjudication and prior authorization automation | Future AGI Agent Command Center | 18+ PHI and PII scanners covering the 18 HIPAA identifiers, BAA available, audit log retention path that meets 45 CFR 164.316(b)(2) six-year minimum |

| Multi-line carrier with multi-LOB dashboard requirement | Portkey | Most fine-grained budget hierarchy plus mature dashboard (verify the Palo Alto Networks integration timeline) |

| Carrier or broker already running Kong for the REST plane | Kong AI Gateway | One control plane across REST and AI; AI plugin family for PII tokenization, semantic caching, and rate limiting |

| Personal-auto carrier running FNOL real-time fraud-scoring | Maxim Bifrost | Strongest published throughput; Apache 2.0; custom DPA on the advanced compliance tier |

| Python-first claims-analytics or actuarial team | LiteLLM (Enterprise) | Broadest provider coverage; commercial release pipeline post-March 2026 CVE |

| Life and health insurer under EU AI Act Annex III high-risk obligations | Future AGI Agent Command Center plus Azure OpenAI | Article 12 logging plus Article 14 human oversight at the same network hop; EU data residency through Azure OpenAI |

| Microsoft 365 plus Azure shop already standardized on Azure OpenAI | Azure OpenAI behind a gateway | DPA via the Microsoft Online Services DPA; image and realtime not yet covered, so gateway-enforced route filtering is required |

| AWS shop on Bedrock with Claude on Bedrock | AWS Bedrock behind a gateway | DPA via the AWS umbrella plus HIPAA-eligible-services list for the Group Health line; gateway adds claim-file PII redaction and per-LOB budgets |

| Early-stage InsurTech evaluating gateways before committing | Future AGI Agent Command Center free tier | Apache 2.0 self-host; upgrade to a Scale tier for the BAA when consumer-affecting decision traffic begins |

Which AI Gateway Is Right for Your Insurance Team in 2026?

Insurance AI in 2026 isn’t a single feature. It’s a stack of NAIC Model Bulletin governance, NYDFS Circular Letter No. 7 disparate-impact testing, EU AI Act Annex III logging and human oversight, HIPAA technical safeguards for the health-insurance line, Colorado Reg 10-1-1 quantitative testing, and state-DOI record-keeping controls riding on top of an AI gateway.

That gateway has to keep claim-file PII (SSN, DOB, policy number, claim number, VIN, NPI, MRN) off the wire, retain a decade-plus of audit logs on the litigation-touched files, survive a Saturday-night provider 5xx without breaking the claims-time settlement clock, and produce a per-decision reconstruction artifact when the state market-conduct examiner asks for it 14 months after the decision was made.

Of the five gateways above, Future AGI Agent Command Center is the strongest pick for the production case where the buying constraint is OpenAI compat drop in plus 18+ built-in claim-file PII scanners.

It also offers per-LOB spend caps plus OpenTelemetry-native underwriter explainability traces plus a self-improving optimizer plus an Apache 2.0 Go binary you can deploy BYOC inside the carrier’s VPC, with an executable BAA available for the Group Health line, an AWS Marketplace listing for one-click procurement, and SOC 2 Type II certified.

Portkey is the right call when a managed cost and audit dashboard is the binding constraint and the Palo Alto Networks integration risk is acceptable. Kong AI Gateway is the right call when the carrier already runs Kong for the REST plane and a single team owns both the REST and AI control planes. Maxim Bifrost is the right call when raw throughput on the FNOL real-time fraud-scoring path is the primary axis. LiteLLM (Enterprise) is the right call for Python-first claims-analytics teams that want commercial release pipeline assurance after the March 2026 PyPI incident.

For deeper reads on the patterns referenced above:

- The Agent Command Center docs for the full gateway feature surface.

- The Future AGI observability docs for the audit log path that anchors NAIC Model Bulletin governance evidence and state-DOI record-keeping retention.

- The Future AGI Protect docs for the runtime guardrail library the gateway plugs into.

- The Future AGI Evaluation docs for the held-out fairness eval that ties to gateway behavior via

span_idand closes the self-improving loop. - The Future AGI tracing product page for the OpenTelemetry-native tracing layer.

- The Future AGI GitHub repo for the Apache 2.0 source.

Try Agent Command Center free. OpenAI-compatible routing, 18+ claim-file PII and PHI guardrails, per-LOB budgets, OpenTelemetry-native traces, and a self-improving optimizer in one Apache 2.0 Go binary, with a BAA available and an AWS Marketplace listing.

Related reading

- Best 5 AI Gateways for Compliance Audit Trails in 2026, the compliance and audit-trail comparison

- Best 5 AI Gateways for LLM Cost Optimization in 2026, the five-layer cost stack and the 2026 trust cohort

- Best 5 AI Gateways for Customer Support in 2026: Latency Budgets, Agent Assist, and Voice AI Passthrough, the customer-support-specific gateway picks

- Best 5 AI Gateways for Cybersecurity in 2026: Prompt Injection Defense, Tenant Isolation, and SOC 2, the cybersecurity-specific gateway picks

Frequently asked questions

What Is the Best AI Gateway for Insurance Compliance in 2026?

Does the NAIC Model Bulletin Apply to LLM Calls Used in Claims or Underwriting?

How Does NYDFS Circular Letter No. 7 (July 11, 2024) Apply to AI in Insurance?

What Does the EU AI Act Require for Insurance AI Systems After August 2, 2026?

How Long Must an Insurer Retain Audit Logs for AI-Assisted Claims Decisions?

How Does an AI Gateway Make an Autonomous Underwriting Decision Explainable?

Which AI Gateways Are Still Safe for Insurance After the 2026 Supply-Chain and Acquisition Events?

Shadow is not canary. Mirror routing with no user effect vs percentage routing with rollback. Score-attached traffic, ACC patterns, gotchas.

Azure OpenAI eval has three Azure-specific axes: deployment-name drift, region-pinning, and Content Safety precision on benign queries. Here's the pattern.

Bedrock's built-in eval is dev-loop only. Score action-group correctness, KB retrieval quality, and guardrail precision/recall on every release.